Diamond Capital Management's Market Commentary

April, 2026

Jeff C. Mantock, CFA, CMT

Vice President, Chief Investment Officer & Manager

Executive Summary:

- Higher oil prices (inflationary pressures) have reduced the prospects for a near-term Fed rate cut.

- Equity valuations have become more reasonable, and profit expectations remain strong.

- The U.S. economy continues to show resilience, and the latest ISM data points to expansion.

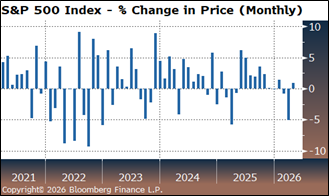

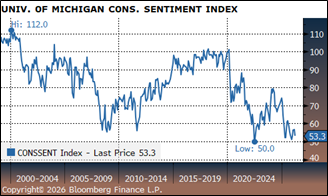

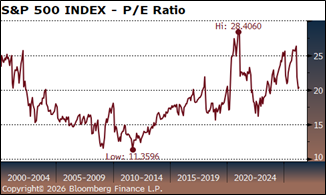

| The financial markets have been heavily influenced by headlines related to the war with Iran. Both stocks and bonds ended the first quarter lower, as higher oil prices and softer labor data raised concerns about inflation and the potential impact on the U.S. economy. The pullback in equities weighed on investor sentiment as higher oil prices also reduced prospects for a near-term Federal Reserve rate cut. Sentiment indicators, often viewed as contrarian signals, remain at depressed levels. We believe investors can look beyond near-term risks and maintain a constructive outlook for equities. Valuations that appeared stretched a few months ago have become more reasonable, profit expectations remain resilient, and optimism around artificial intelligence continues to support the longer-term growth narrative. Historically, markets have also tended to rebound following geopolitical shocks. |

|

|

The S&P 500 posted its steepest monthly decline since March 2025. Investor anxiety was evident in the CBOE Volatility Index (VIX), which rose above 30 near the end of the month. In more stable markets, this indicator typically trades in the mid-teens. The VIX generally moves inversely to the S&P 500 Index, rising as investors increase their demand for put options to protect against downside risk. Historically, sharp spikes in volatility have often created attractive entry points for disciplined, long-term investors who can tolerate short-term fluctuations and capitalize on prices pressured by fear.

|

|

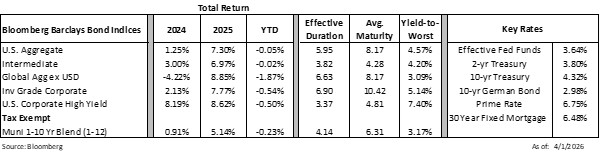

| The U.S. economy continues to show resilience, with demand driven primarily by services even as inflation and rate uncertainty remain key crosscurrents. The latest ISM data point to expansion across both major sectors: the ISM Manufacturing PMI for March was 52.3 (above the 50 breakeven level), while the ISM Services PMI for February rose to 56.1, signaling a faster pace of growth in the largest part of the economy. Together, these readings suggest activity remains solid and broad-based, though the policy outlook will stay sensitive to any renewed price pressures. |  |

The information and material contained herein is provided solely for general information purposes. This material is not intended to be investment advice nor is this information intended as an offer or solicitation for the purchase or sale of any security or other financial instrument. Any opinions expressed herein are given in good faith, are subject to change without notice, and are only current as of the stated date of their issue. Certain sections of this publication contain forward-looking statements that are based on the reasonable expectations, estimates, projections, and assumptions of the authors, but forward-looking statements are not guarantees of future performance and involve risks and uncertainties. Investment ideas and strategies presented may not be suitable for all investors. No responsibility or liability is assumed by The National Bank of Indianapolis, or its affiliates for any loss that may directly or indirectly result from use of information, commentary, or opinions in this publication by you or any other person.